What are the Types of Health Insurance Plans Available in USA?

Health insurance is an essential aspect of healthcare in the USA. With the rising costs of medical treatments, having a health insurance plan is crucial to ensure access to quality healthcare without incurring significant financial burden. However, there are various types of health insurance plans available in the USA, each with its own features and benefits.

One of the most common types of health insurance plans in the USA is the Preferred Provider Organization (PPO) plan. This type of plan offers a network of healthcare providers that have agreed to provide services at a discounted rate to plan members. PPO plans offer flexibility in choosing healthcare providers, allowing individuals to seek care both in-network and out-of-network, although out-of-network care may result in higher out-of-pocket costs.

Another type of health insurance plan commonly found in the USA is the Health Maintenance Organization (HMO) plan. HMO plans typically require individuals to select a primary care physician (PCP) who coordinates all their healthcare needs. PCPs act as gatekeepers, providing referrals to specialists within the network when necessary. HMO plans generally have lower out-of-pocket costs compared to PPO plans but offer less flexibility in choosing healthcare providers.

Additionally, there are High Deductible Health Plans (HDHP) available in the USA, which are often paired with Health Savings Accounts (HSA). HDHPs have higher deductibles compared to traditional health insurance plans but offer lower monthly premiums. HSAs allow individuals to save pre-tax money to be used for qualified medical expenses. This combination provides individuals with greater control over their healthcare expenses and potential tax benefits.

Understanding Health Insurance

Health insurance is a type of insurance that provides coverage for medical expenses incurred by individuals. It is an essential aspect of healthcare in the United States, where the cost of medical treatment can be very high. Understanding health insurance is crucial for individuals to ensure they have access to necessary healthcare services without facing financial burdens.

There are different types of health insurance plans available in the USA, each offering different levels of coverage and benefits. These plans include employer-sponsored plans, government-funded plans like Medicare and Medicaid, and individual plans purchased directly by individuals.

Employer-sponsored health insurance plans are provided by employers to their employees as part of their employee benefits package. These plans often offer comprehensive coverage and are typically more affordable compared to individual plans. However, the coverage and benefits may vary depending on the employer and the specific plan.

Government-funded health insurance plans, such as Medicare and Medicaid, are designed to provide healthcare coverage to specific groups of people. Medicare is primarily for individuals aged 65 and older, while Medicaid is for low-income individuals and families. These plans are funded by the government and offer different levels of coverage and benefits.

Individual health insurance plans are purchased directly by individuals from insurance companies. These plans offer flexibility in terms of coverage options and providers but can be more expensive compared to employer-sponsored plans. Individuals can choose from a variety of plans with different coverage levels and premiums to suit their specific healthcare needs and budget.

Understanding the different types of health insurance plans available in the USA is important for individuals to make informed decisions about their healthcare coverage. It is advisable to carefully review the coverage, benefits, and costs associated with each plan before choosing the most suitable option.

The Importance of Health Insurance

Health insurance is of great importance in the USA, where there are various types of insurance plans available. It provides individuals and families with financial protection against the high costs of medical care and ensures access to necessary healthcare services.

One of the key benefits of health insurance is that it helps to cover the expenses related to preventive care. Regular check-ups, vaccinations, and screenings are essential for maintaining good health and preventing serious illnesses. With health insurance, individuals can receive these preventive services at little to no cost, encouraging them to prioritize their health and well-being.

Furthermore, health insurance provides coverage for medical emergencies. Accidents and unexpected health issues can happen at any time, and having insurance helps to alleviate the financial burden associated with emergency medical care. Whether it’s a sudden illness, a broken bone, or a need for surgery, health insurance ensures that individuals receive the necessary treatment without incurring overwhelming medical bills.

In addition to preventive care and emergency coverage, health insurance also offers access to a wide network of healthcare providers. Insurance plans often have a list of preferred providers, including doctors, hospitals, and specialists, with whom they have negotiated lower rates. This network ensures that individuals can receive quality care from reputable healthcare professionals, without having to worry about finding providers or paying exorbitant out-of-pocket costs.

Overall, health insurance plays a crucial role in promoting and maintaining the well-being of individuals and families in the USA. It provides financial protection, access to preventive care, coverage for emergencies, and access to a network of healthcare providers. With the variety of insurance plans available, individuals can choose the one that best suits their needs and ensures that they receive the necessary medical care when they need it the most.

Employer-Sponsored Health Insurance

Employer-sponsored health insurance is one of the most common types of health insurance plans available in the USA. This type of insurance is provided by employers to their employees as part of their benefits package. It is a way for employers to help their employees access healthcare services and manage their health expenses.

Employer-sponsored health insurance plans vary in terms of coverage and cost. Some employers offer comprehensive plans that cover a wide range of medical services, including doctor visits, hospital stays, and prescription medications. Other employers may offer more basic plans that only cover essential healthcare services.

One of the advantages of employer-sponsored health insurance is that the cost is often shared between the employer and the employee. Employers typically pay a portion of the monthly premiums, while employees are responsible for paying the remaining portion. This can make health insurance more affordable for employees.

Another advantage of employer-sponsored health insurance is that it is usually offered to all full-time employees, regardless of their health status. This means that individuals with pre-existing conditions or chronic illnesses can still access health insurance through their employer. However, the availability of employer-sponsored health insurance may vary depending on the size of the company and its financial resources.

In conclusion, employer-sponsored health insurance is a common type of health insurance available in the USA. It is provided by employers to their employees as part of their benefits package and helps employees access healthcare services. The coverage and cost of these plans can vary, but they often provide a shared cost between the employer and the employee. This type of insurance is typically offered to all full-time employees, making it accessible to individuals with pre-existing conditions or chronic illnesses.

Individual Health Insurance

Individual health insurance is a type of health insurance that is purchased by an individual, rather than being provided by an employer. It is designed to provide coverage for an individual’s medical expenses and can be tailored to meet their specific needs.

There are several types of individual health insurance plans available, each with its own set of benefits and coverage options. These plans can be categorized into two main types: fee-for-service and managed care.

Fee-for-service plans, also known as indemnity plans, allow individuals to choose their healthcare providers and have more freedom in selecting the services they receive. These plans typically have higher out-of-pocket costs, such as deductibles and co-payments, but offer greater flexibility in terms of coverage.

Managed care plans, on the other hand, involve a network of healthcare providers who have agreed to provide services at a discounted rate. These plans include health maintenance organizations (HMOs), preferred provider organizations (PPOs), and point of service (POS) plans. Managed care plans often require individuals to choose a primary care physician and obtain referrals for specialized care.

Individual health insurance plans can vary in terms of coverage and cost, so it’s important for individuals to carefully review their options and consider their healthcare needs before selecting a plan. It’s also worth noting that individual health insurance plans are subject to certain regulations and requirements, such as the Affordable Care Act’s mandate for essential health benefits.

Group Health Insurance

Group health insurance is a type of health insurance available in the USA that covers a group of people, typically employees of a company or members of an organization. It is an insurance plan that is purchased by an employer or organization and offered to eligible individuals as a benefit.

There are different types of group health insurance plans available, including employer-sponsored plans, association health plans, and government-sponsored plans. Employer-sponsored plans are the most common type of group health insurance in the USA, where employers offer health insurance coverage to their employees as part of their employee benefits package.

Group health insurance provides coverage for a wide range of health services, including doctor visits, hospital stays, prescription medications, preventive care, and more. The coverage and benefits vary depending on the specific plan and the insurance provider.

One of the advantages of group health insurance is that it often offers lower premiums compared to individual health insurance plans. This is because the risk is spread across a larger group of people, which can result in lower costs for the insurance provider. Additionally, group health insurance plans may offer more comprehensive coverage and additional benefits compared to individual plans.

Overall, group health insurance is a valuable option for individuals in the USA who are looking for health insurance coverage. It provides access to a wide range of health services and can offer cost savings compared to individual plans. Whether through an employer or organization, group health insurance offers an important safety net for individuals and their families.

Medicare

Medicare is a government health insurance program in the USA that provides coverage for individuals who are 65 years old or older, as well as for certain younger individuals with disabilities. It is divided into different parts, each covering specific services and expenses.

There are several types of Medicare plans available, including:

- Medicare Part A: This covers inpatient hospital stays, skilled nursing facility care, and some home health care services.

- Medicare Part B: This covers outpatient medical services, such as doctor visits, preventive care, and durable medical equipment.

- Medicare Part C: Also known as Medicare Advantage, these plans are offered by private insurance companies and provide all the benefits of Part A and Part B, as well as additional coverage, such as prescription drugs and dental services.

- Medicare Part D: This is prescription drug coverage and is available as a standalone plan or as part of a Medicare Advantage plan.

Medicare provides essential health coverage for seniors and individuals with disabilities in the USA. It is important for individuals to understand the different parts of Medicare and choose the plan that best suits their needs.

Medicaid

Medicaid is a type of health insurance program in the USA that is designed to provide coverage for low-income individuals and families. It is jointly funded by the federal government and individual states, with each state having its own eligibility criteria and benefits.

There are different types of Medicaid plans available, depending on the specific needs of the individual or family. These plans can include coverage for doctor visits, hospital stays, prescription medications, and preventive care. Some plans may also offer additional services such as dental and vision care.

Medicaid eligibility is based on income and other factors, such as age, disability status, and family size. The program is intended to provide coverage for those who cannot afford private health insurance or do not have access to employer-sponsored coverage.

Medicaid is an important safety net for millions of Americans, providing them with access to essential health care services. It plays a crucial role in ensuring that low-income individuals and families can receive the medical care they need to stay healthy and manage chronic conditions.

Overall, Medicaid is a vital component of the US healthcare system, helping to bridge the gap in health insurance coverage for those who might otherwise go without necessary medical care.

Children’s Health Insurance Program (CHIP)

The Children’s Health Insurance Program (CHIP) is one of the types of health insurance available in the USA. It is a government program that provides low-cost or free health coverage to children in low-income families. CHIP is designed to ensure that children have access to necessary healthcare services, including doctor visits, immunizations, prescriptions, dental care, and hospital care.

CHIP is administered by individual states, and eligibility requirements may vary. Generally, children from families with limited income who do not qualify for Medicaid are eligible for CHIP. The program covers children up to the age of 19, and some states also offer coverage for pregnant women. CHIP provides comprehensive coverage, and families enrolled in the program may have to pay monthly premiums, copayments, or other costs depending on their income level.

CHIP offers a wide range of benefits to ensure that children receive the care they need. These benefits may include preventive services such as regular check-ups and screenings, as well as treatment for illnesses and injuries. Prescription medications, mental health services, and substance abuse treatment may also be covered. Additionally, CHIP may provide access to specialized care for children with chronic conditions or disabilities.

Enrolling in CHIP is a simple process, and families can apply online, by phone, or in person at their state’s Medicaid or CHIP office. Once eligible, children can receive coverage for a full year, and renewal is typically automatic. The program is an essential resource for families who may not have access to employer-sponsored health insurance or who cannot afford private insurance plans.

In summary, the Children’s Health Insurance Program (CHIP) is a vital component of the healthcare system in the USA. It provides low-cost or free health coverage to children from low-income families, ensuring they have access to necessary healthcare services. CHIP offers comprehensive benefits and is administered by individual states. Eligible families can apply easily, and the program provides coverage for a full year. CHIP plays a crucial role in ensuring that all children have the opportunity to lead healthy lives.

Health Maintenance Organization (HMO) Plans

Health Maintenance Organization (HMO) plans are a type of health insurance plan available in the USA. These plans offer a comprehensive range of healthcare services to individuals and families. HMO plans focus on preventive care and emphasize the importance of regular check-ups and screenings to maintain good health.

Under an HMO plan, individuals are required to choose a primary care physician (PCP) who acts as a gatekeeper for all their healthcare needs. The PCP coordinates the individual’s care and provides referrals to specialists when necessary. This helps to ensure that healthcare services are delivered in a coordinated and cost-effective manner.

One of the key features of HMO plans is that they often have a network of healthcare providers that individuals must use in order to receive coverage. This network typically includes hospitals, doctors, and other healthcare professionals who have agreed to provide services at a reduced rate to HMO plan members.

In addition to the network requirement, HMO plans usually require individuals to obtain a referral from their PCP before seeing a specialist. This helps to control costs and ensure that individuals receive appropriate care.

Overall, HMO plans offer a cost-effective and coordinated approach to healthcare. They are a popular choice for individuals and families who are looking for comprehensive coverage and are willing to work within a network of healthcare providers.

Preferred Provider Organization (PPO) Plans

Preferred Provider Organization (PPO) plans are one of the many types of health insurance plans available in the United States. These plans offer a network of healthcare providers that have agreed to provide services at discounted rates to members of the plan.

With PPO plans, members have the flexibility to choose their healthcare providers from within the network or outside of it. If a member chooses to receive care from a provider outside of the network, they may have to pay higher out-of-pocket costs. However, PPO plans typically offer some coverage for out-of-network care, which can be beneficial for individuals who have specific healthcare needs or prefer to see a provider who is not in the network.

One advantage of PPO plans is that members do not need a referral to see a specialist. They have the freedom to schedule appointments with specialists directly, without having to first see a primary care physician. This can be particularly advantageous for individuals who require specialized care for chronic conditions or complex medical issues.

Another feature of PPO plans is that they generally do not require members to choose a primary care physician. This means that members have the flexibility to see different doctors for different healthcare needs, without the need for a gatekeeper. This can be beneficial for individuals who prefer to have more control over their healthcare decisions and want the freedom to choose their providers.

Overall, PPO plans offer a balance between flexibility and cost savings. They provide a wide range of healthcare options and allow members to seek care from both in-network and out-of-network providers. However, it’s important for individuals to carefully review the details of the plan, including the network of providers and the coverage for out-of-network care, in order to make an informed decision about their healthcare coverage.

Exclusive Provider Organization (EPO) Plans

An Exclusive Provider Organization (EPO) plan is a type of health insurance plan available in the USA. It falls under the category of managed care plans, which aim to provide cost-effective healthcare options to individuals and families.

EPO plans offer a network of healthcare providers, including doctors, specialists, and hospitals, that policyholders must use in order to receive coverage. These plans do not typically require a referral from a primary care physician to see a specialist, giving policyholders more flexibility in choosing their healthcare providers.

One of the key features of EPO plans is that they do not provide coverage for out-of-network healthcare services, except in cases of emergency. This means that if a policyholder seeks care from a provider outside of the EPO network, they will be responsible for paying the full cost of the services.

However, EPO plans often have lower monthly premiums compared to other types of health insurance plans, such as Preferred Provider Organization (PPO) plans. This can make them an attractive option for individuals and families who want to save on their healthcare costs.

It is important for individuals considering an EPO plan to carefully review the network of providers to ensure that their preferred doctors and hospitals are included. Additionally, policyholders should be aware of the restrictions on out-of-network coverage and be prepared to pay out-of-pocket for any services received outside of the network.

Point of Service (POS) Plans

Point of Service (POS) plans are available in the USA as one of the different types of health insurance plans. These plans provide a combination of features from both Health Maintenance Organization (HMO) and Preferred Provider Organization (PPO) plans. POS plans offer more flexibility compared to HMO plans, allowing individuals to choose healthcare providers both within and outside the plan’s network.

With a POS plan, individuals have a primary care physician (PCP) who manages their healthcare and refers them to specialists when needed. When visiting an in-network provider, individuals pay lower out-of-pocket costs, such as copayments or coinsurance. However, if they choose to receive care from an out-of-network provider, they may have to pay higher costs.

POS plans typically require individuals to obtain a referral from their PCP before seeking specialized care. This helps to coordinate healthcare and ensure that individuals receive appropriate and necessary treatments. However, in emergency situations, individuals can seek care from any provider without a referral.

Overall, POS plans offer a balance between cost savings and flexibility. They are suitable for individuals who want the option to choose healthcare providers outside of the network while still enjoying the benefits of lower costs when staying within the network.

High-Deductible Health Plans (HDHP)

A High-Deductible Health Plan (HDHP) is a type of health insurance plan that has a higher deductible compared to other available plans. It is designed to provide coverage for major health expenses while keeping monthly premiums lower.

With an HDHP, individuals are responsible for paying a higher deductible amount before the insurance company starts covering the costs. This deductible is usually higher than what is typically found in other types of health insurance plans. The idea behind an HDHP is to encourage individuals to become more cost-conscious and responsible for their health care expenses.

Although the upfront costs may be higher with an HDHP, this type of plan can be beneficial for those who are generally healthy and do not anticipate needing frequent or expensive medical care. It can also be a good option for those who prefer to have lower monthly premiums and are willing to take on more financial responsibility for their health care expenses.

One advantage of an HDHP is that it can be paired with a Health Savings Account (HSA). An HSA is a tax-advantaged savings account that allows individuals to set aside money to pay for qualified medical expenses. Contributions to an HSA are tax-deductible, and any unused funds can be rolled over from year to year. This can help individuals save money on their taxes and build up a fund for future medical expenses.

Overall, High-Deductible Health Plans (HDHPs) are one of the available types of health insurance plans in the USA. They can be a cost-effective option for individuals who are generally healthy and prefer lower monthly premiums. However, it is important to carefully consider your own health needs and financial situation before choosing a plan.

Health Savings Account (HSA)

A Health Savings Account (HSA) is a type of health insurance plan available in the USA. It is designed to help individuals save and pay for medical expenses. HSAs are typically paired with high-deductible health insurance plans, which means that individuals must pay a certain amount out of pocket before their insurance coverage kicks in.

With an HSA, individuals can contribute pre-tax money into their account, which can then be used to pay for qualified medical expenses. This includes expenses such as doctor visits, prescription medications, and hospital stays. The money in an HSA can also be invested, allowing it to grow over time and be used for future medical expenses.

One of the main benefits of an HSA is the tax advantages it offers. Contributions to an HSA are tax-deductible, and any interest or investment gains are tax-free. Additionally, withdrawals from an HSA for qualified medical expenses are also tax-free. This makes an HSA a valuable tool for individuals looking to save money on their healthcare costs.

It’s important to note that HSAs have certain eligibility requirements. To be eligible for an HSA, individuals must have a high-deductible health insurance plan, not be enrolled in Medicare, and not be claimed as a dependent on someone else’s tax return. Employers may also offer HSAs as part of their employee benefits package.

In summary, a Health Savings Account (HSA) is a type of health insurance plan that allows individuals to save and pay for medical expenses. It offers tax advantages and is typically paired with a high-deductible health insurance plan. HSAs are a valuable tool for individuals looking to save money on their healthcare costs in the USA.

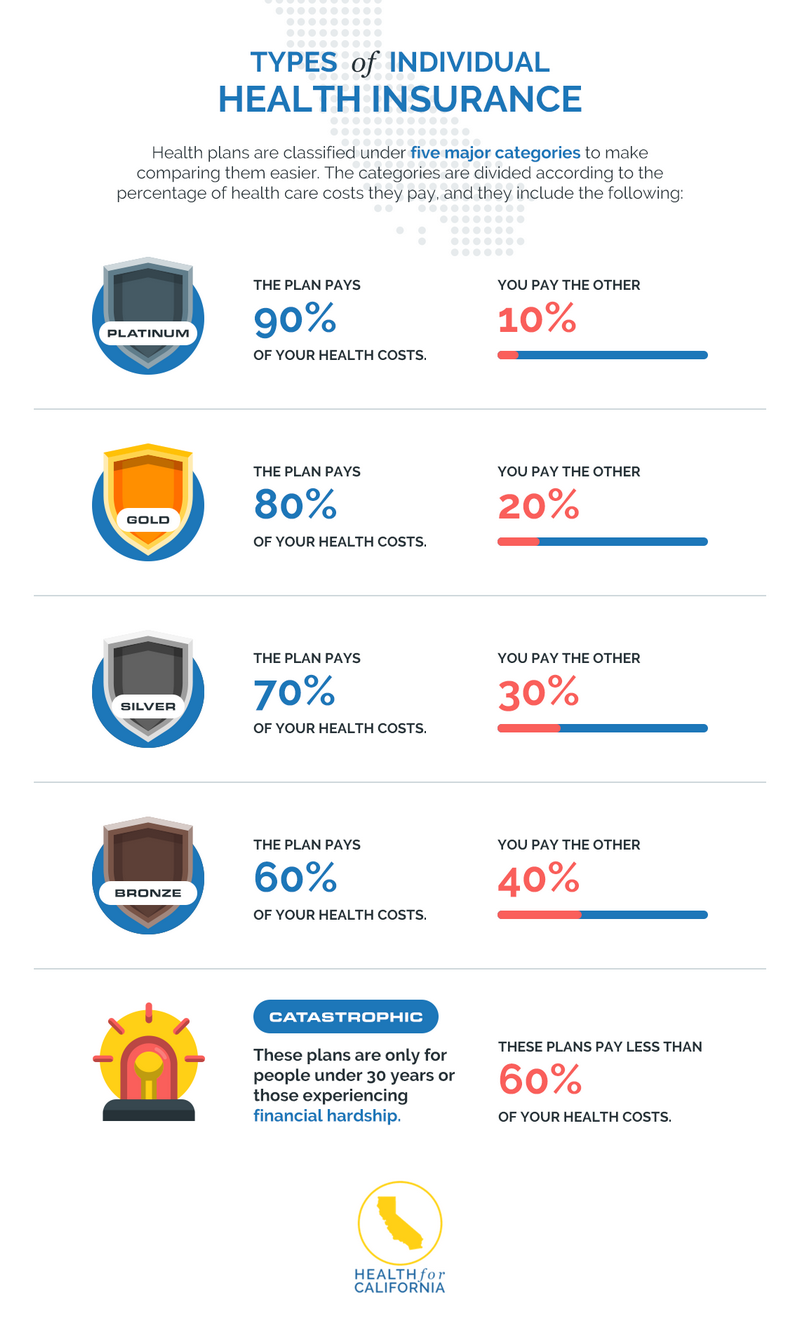

Catastrophic Health Insurance Plans

Catastrophic health insurance plans are a type of insurance available in the USA. These plans are designed to provide coverage for major medical expenses in the event of a serious illness or injury. They are typically available to individuals under the age of 30 or those who qualify for a hardship exemption.

Unlike other types of health insurance plans, catastrophic plans have lower monthly premiums but higher deductibles. This means that individuals will have to pay a larger portion of their medical expenses out of pocket before the insurance coverage kicks in. However, once the deductible is met, the plan will usually cover 100% of the costs for essential health benefits.

Catastrophic health insurance plans are a good option for individuals who are generally healthy and do not require frequent medical care. They provide financial protection in case of a major health crisis, such as a serious accident or the diagnosis of a severe illness. These plans also typically include preventive services at no additional cost, such as vaccinations and screenings.

It’s important to note that catastrophic health insurance plans do not meet the requirements of the Affordable Care Act (ACA) and do not qualify for premium tax credits or cost-sharing reductions. They also do not cover services that are not considered essential health benefits, such as maternity care or prescription drugs. Individuals considering a catastrophic plan should carefully evaluate their healthcare needs and budget before making a decision.

Short-Term Health Insurance Plans

Short-term health insurance plans are a type of insurance coverage that is available in the USA. These plans are designed to provide temporary health coverage for individuals who are in between jobs, waiting for employer-sponsored coverage to start, or simply need coverage for a short period of time.

Short-term health insurance plans typically offer coverage for a limited duration, ranging from a few months to a year. They are often more affordable compared to long-term health insurance plans, making them a popular choice for individuals who need temporary coverage.

However, it’s important to note that short-term health insurance plans may not provide the same level of coverage as long-term plans. They may have limitations on pre-existing conditions, and they may not cover certain services or treatments. It’s important for individuals to carefully review the terms and conditions of a short-term health insurance plan before enrolling.

Short-term health insurance plans are available from various insurance providers in the USA. Individuals can compare different plans and choose the one that best fits their needs and budget. It’s important to consider factors such as the duration of coverage, the cost of premiums, and the level of coverage provided when selecting a short-term health insurance plan.

In conclusion, short-term health insurance plans are a flexible and affordable option for individuals who need temporary health coverage in the USA. While they may not offer the same level of coverage as long-term plans, they can provide valuable protection during transitional periods or when other coverage options are not available.

Choosing the Right Health Insurance Plan

When it comes to health insurance in the USA, there are various types of plans available. It is important to carefully consider your options and choose the right plan that suits your needs and budget.

1. Health Maintenance Organization (HMO) Plans: HMO plans require you to choose a primary care physician (PCP) who will coordinate your healthcare. You must get a referral from your PCP to see specialists. These plans generally have lower monthly premiums and out-of-pocket costs.

2. Preferred Provider Organization (PPO) Plans: PPO plans offer more flexibility in choosing healthcare providers. You can see any doctor or specialist without a referral, but you will pay less if you choose providers within the network. PPO plans typically have higher premiums and out-of-pocket costs.

3. Exclusive Provider Organization (EPO) Plans: EPO plans are similar to PPO plans but do not cover out-of-network care, except in emergencies. These plans may have lower monthly premiums compared to PPO plans.

4. Point of Service (POS) Plans: POS plans combine elements of HMO and PPO plans. You must choose a primary care physician, but you have the option to see out-of-network providers at a higher cost. POS plans generally have higher monthly premiums.

5. Catastrophic Health Insurance Plans: Catastrophic plans are designed for individuals under 30 or those who qualify for a hardship exemption. These plans have low monthly premiums but high deductibles. They provide coverage for emergencies and essential health benefits.

Before making a decision, it is important to carefully review the details of each plan, including the coverage, network of providers, premiums, deductibles, and out-of-pocket costs. Consider your healthcare needs, such as prescription medications, regular doctor visits, and any ongoing treatments, to choose a plan that provides adequate coverage.

Question-answer:

What are the different types of health insurance plans available in the USA?

There are several different types of health insurance plans available in the USA, including HMOs, PPOs, EPOs, and POS plans. Each type of plan has its own unique features and benefits.

What is an HMO health insurance plan?

An HMO, or Health Maintenance Organization, is a type of health insurance plan that typically requires members to choose a primary care physician (PCP) who coordinates their healthcare. HMOs generally have lower out-of-pocket costs but require members to receive care within a network of providers.

What is a PPO health insurance plan?

A PPO, or Preferred Provider Organization, is a type of health insurance plan that allows me